[ad_1]

Listed here are 5 observations about current traits in financial coverage:

1. The Fed would like to keep away from any additional improve in rates of interest. This psychological aversion to rate of interest will increase in not rational, and it truly makes it extra possible that the Fed will discover it needed to boost rates of interest even additional. That’s as a result of this kind of “reversal aversion” is itself a type of ahead steering, which makes financial coverage extra clumsy. It will increase the chance that disinflation will reverse course, requiring additional charge will increase.

2. I’ve seen claims that Jay Powell privately prefers Biden to Trump. Folks usually cite the truth that he refused to chop rates of interest as usually as Trump would have preferred, and that he avoided tightening financial coverage in late 2021 as Biden was contemplating whether or not to re-appoint him as Fed chair. I don’t know if these accusations of political favoritism are true (I’m skeptical), but when true it implies that Powell ended up drastically serving to Trump and hurting Biden, even whereas showing to be making an attempt to do the alternative.

The message right here is obvious. Folks fear an important deal about political bias. However with regards to financial coverage, coverage errors are a far better downside than coverage bias.

3. Mohamed A. El-Erian has a brand new essay in Bloomberg:

Quite than keep a coverage response operate anchored by extreme dependence on backward-looking knowledge, the Fed can be nicely suggested to take this chance to undertake a belated pivot to a extra strategic view of secular prospects. Such a pivot would acknowledge that the optimum medium-term inflation stage for the US is nearer to three% and, as such, give policymakers the flexibleness to not overreact to the most recent inflation prints.

As I detailed in a column final month, this path wouldn’t contain an express and quick change within the inflation goal given the extent to which the Fed has overshot it within the final three years. As an alternative, it could be a gradual development. Particularly, the Fed “would first push out expectations on the timing of the journey to 2% after which, nicely down the street, transition to an inflation goal primarily based on a spread, say 2-3%.” . . .

Whereas not with out dangers, such a coverage strategy would end in a greater general consequence for the economic system and monetary stability than one which sees the Fed run an excessively tight financial coverage.

I agree that this may end in a greater consequence for the economic system over the following few years. However I don’t consider that it’s a good suggestion. Ideally, the Fed would shift to a 4% NGDP goal. But when they insist on sticking with inflation focusing on, they need to keep at 2%. It is a traditional instance of the time inconsistency downside. One of the best coverage for the following few years will not be all the time the very best long-term technique. In the long term, there are large positive aspects from creating a transparent rule and sticking with it.

4. Brad Setser expresses some broadly held views relating to China’s change charge coverage:

China must search for insurance policies that transfer it nearer towards e book inside and exterior stability – and that (uncomfortably) means limiting the usage of traditional financial coverage instruments.

However it is usually affordable that China made an actual effort to make use of its home coverage area to help its personal restoration—and to date it has not been prepared to supply direct help to decrease earnings households, or to contemplate reforms to its exceptionally regressive tax system. Logan Wright and Daniel Rosen foot stomped these factors in a current article in International Affairs.

Finally, after all, China units its personal change charge coverage; it has an extended historical past of ignoring exterior recommendation that goes in opposition to its self-perception of its personal pursuits. However there isn’t a motive why China’s commerce companions ought to encourage China to maneuver towards extra flexibility proper now, when it could solely assist China export extra of its personal manufactures to a reluctant world. Pragmatism ought to rule.

I’ve precisely the alternative view. China ought to keep away from fiscal stimulus and as an alternative depend on financial stimulus, even when this ends in foreign money depreciation. I additionally doubt that this kind of yuan depreciation would end in a bigger Chinese language commerce surplus. Financial stimulus would possible enhance Chinese language funding, which tends to decrease its present account surplus. It may additionally enhance home saving, however in all probability by a smaller quantity. In different phrases the substitution impact ensuing from a weaker yen is prone to be weaker than the earnings impact ensuing from simple cash boosting GDP progress.

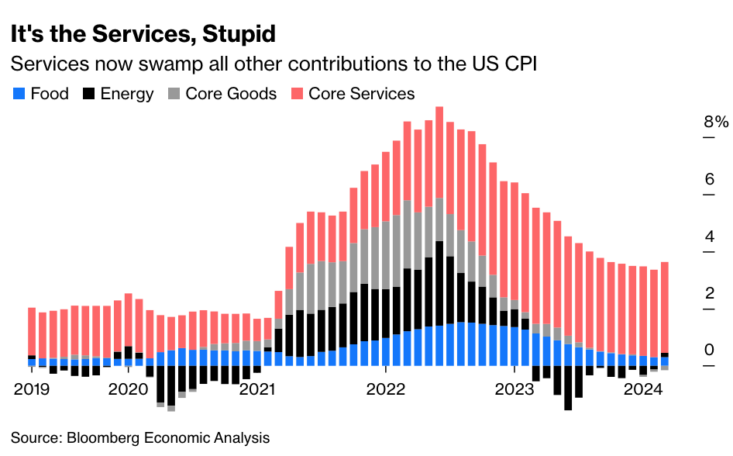

5. John Authers at Bloomberg has an fascinating graph exhibiting the contribution of 4 key sectors to the general (12-month) charge of CPI inflation:

Meals, vitality and core items are rather more strongly affected by “provide shocks” than are companies. However financial coverage does impression even the costs of those items. Thus you’ll be able to consider the purple space (companies) as virtually fully reflecting financial coverage, and fluctuations within the black, blue and gray areas as reflecting a mixture of financial (demand aspect) and provide aspect elements.

Service sector inflation stopped enhancing after October 2023, which is a worrisome pattern.

[ad_2]

Source link